Hi,

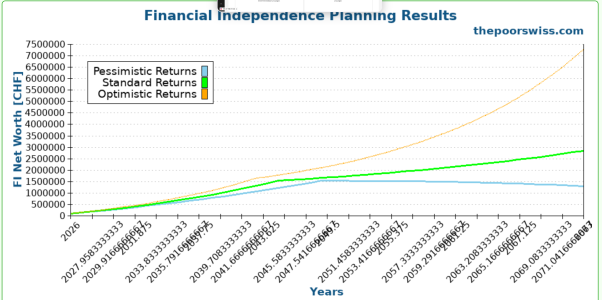

I am trying to build a new calculator to do some Financial Independence planning. The goal of this is to accurately plan when we can reach FI and whether our plan holds in retirement.

I have reached a decent first version:

thepoorswiss.com

thepoorswiss.com

I would appreciate any feedback:

* Features to add

* Things that don't work

* How to improve it

Thanks

I am trying to build a new calculator to do some Financial Independence planning. The goal of this is to accurately plan when we can reach FI and whether our plan holds in retirement.

I have reached a decent first version:

Financial Independence Planner - The Poor Swiss

The goal of the Financial Independence (FI) planner is to help you plan your early retirement, from now until the end of the retirement. It is meant to be an

thepoorswiss.com

I would appreciate any feedback:

* Features to add

* Things that don't work

* How to improve it

Thanks

")

") Would it be possible to change that so that only the full year is visible, with no point and no decimals.

Would it be possible to change that so that only the full year is visible, with no point and no decimals.