I was wondering, specifically for Swiss investors:

- If your goal is to FIRE and live off of your investments for 50 years, how high could your annual deduction be? Would 3.5% be too risky?

- How can you prepare for market downturns? Would you keep cash/bond buckets so you don't have to sell stock shares when the market is doing poorly? If so, would it suffice to keep around 2-3 years of (potentially very) frugal living in there?

- If you don't necessarily want to stay in Switzerland: what are the best countries to do this in? Or would you just stay a resident of Switzerland, but "country-hop"? Would that even work / make sense, tax-wise etc?

- What are the cheapest countries to live in comfortably (and safely)? If you don't need much and just want to chill and let your portfolio grow a bit more, while also living off of a part of the earnings: what place on earth would allow you to spend the least?

- How would you deal with housing? Buying a property in Switzerland seems excessively expensive. But can you even be a resident if you don't permanently rent here nor own a place? And if you move to a different country altogether: would you buy a house there, or would renting make more sense financially?

1. I like to be conservative and I've always aimed at a "dynamic" 3.5%, with that I want to mean always the same percentage, but the real sum changes along with the nominal size of my portfolio. If my wealth goes from 2M to 1,5M, then the 3.5% goes from 70k to 52.5k. I know it's not for everybody, but there are also other options like setting a max nominal change per year (let's say, never reduce/raise more than a 10% from last year). Every option has its implications on the sustainability of your withdrawal ratio, that's why I encourage you to play with withdrawal ratios calcs.

Also, the % that you can withdraw is very affected by your total portfolio volatility, the less volatile the more you can withdraw as a % (ceteris paribus).

2. Gold (decorrelated asset). Secondary income sources (paid hobbies, part time jobs, etc). Life diversification (if you have or can have a source of income/job in your country, then don't over-invest in that country, or a crisis will hit you double).

I don't really like bonds and it's nice that you put it in the same bucket as cash, because both are almost the same thing: a passive from the State. They share the same fragility, and no bond is going to protect you if the crisis or the stagnation comes from inflation. And governments don't stop increasing their debt in the long term (there is a political trap of incentives that provokes so), so...

3 & 4. Tbh I don't know, it may be very personal, for example, living in a less safe country could be not as unsafe if you know the place, the culture, etc (for example you or your partner being from there). Also take into consideration where you want to raise/educate your children, or what kind/quality of medical care you want when you will most need it (when you get your 60+ years), is your family close? etc etc.. There's plenty of "cheap" countries, but not everything you spend is money. Difficult topic, and very individual answers for everyone I supose.

5. I'm far from being swiss-housing expert and please somebody correct me if I'm mistaken: but there's apparently a premium in the multiplier of the houses here (like the PER buf for houses) due to the low interests of the CHF. I mean, yeah you pay a higher price, but at the end you dont necessarily pay a lot more (if you buy with mortgage), because interests are low and in the long term they are a big part of the final sum you pay for a house. That's why, compared to other countries, rents look "cheap" in relation with the price of buying, and also why buying doesn't give you very interesting yields from renting.

About moving, finnancially speaking is difficult that real estate (as average) surpases the rent of stocks, specially if you don't deeply know the country or even the area.

My thoughts on this is: when you buy a house you protect yourself from the rise of rent prices. Just like buying live chickens protects you from the rise of eggs' price, because now you produce the ones you consume. So now you produce "shelter" in that place. So if you know you want to always live there, owning could make a lot of sense, because you dont care about the fluctuations of the price of the house if you are never going to sell, but you care about the fluctuations of the price of renting. It would be like buying a future contract and seal a deal with current prices.

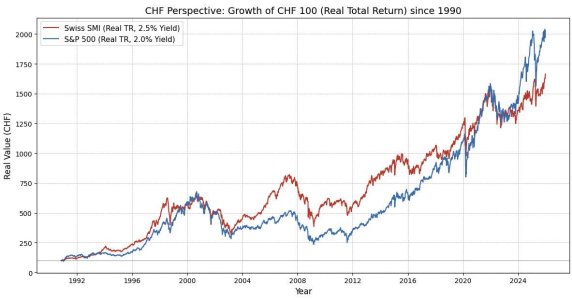

About your conversation with the USD.. I'm not really that concerned about the depreciation of any currency as long as I don't have much cash in any. We are long term investors, and relative currency depretiations in the long term either settle, becoming pure inflation (real depreciation of the currency), or reverse. So if you own stocks in USD you don't need to worry about the USD, the asset you own is the stock, the company, not the currency. In case of inflation they'll raise more or less the same as inflation does, just look how stocks in USD have raised after the sudden USD depreciation, and also every thing sold in USD (for instance, a USD ETF of Australian stocks), and then look at the same assets in EUR or CHF.