Ex Pat

Member

Hey,

My IPS says that I should start adding bonds into my portfolio at the end of they year.

What I put in my IPS (and now I have to actually understand and realize what this means in practice) is :

And I also got this advice from @Rttm

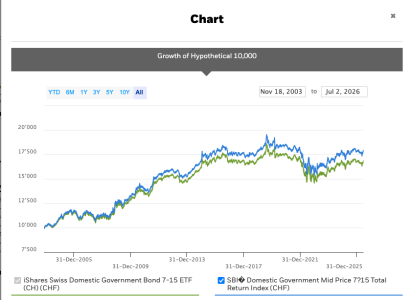

The problem that I have is that I don't know where to start, and what those "CHF-denominated, investment-grade, via a low-cost broad ETF" bonds should look like.

Is it better to look only in government bonds, or also industrial bonds because Swiss companies tend to be stable?

My IPS says that I should start adding bonds into my portfolio at the end of they year.

What I put in my IPS (and now I have to actually understand and realize what this means in practice) is :

Bonds will be CHF-denominated, investment-grade, via a low-cost broad ETF with short-to-intermediate duration.

And I also got this advice from @Rttm

Uncorrelated assets combined with regular rebalancing lead to a much more stable portfolio (reducing volatility and, consequently, making a "lost decade" less likely), while also theoretically improving performance (see Shannon’s Demon: https://www.richmondquant.com/news/...tfolio-returns-can-be-created-out-of-thin-air).

The problem that I have is that I don't know where to start, and what those "CHF-denominated, investment-grade, via a low-cost broad ETF" bonds should look like.

Is it better to look only in government bonds, or also industrial bonds because Swiss companies tend to be stable?

")